Monika’s story

After an MA in Economics from the Delhi School of Economics, I realised that I knew nothing about money. My entire salary from my first job in a business magazine would go into auto fares (so that I did not have to travel by DTC buses – the idea was not luxury, just escape from creepy men who stood too close), eating out and clothes.

The extent of my money illiteracy came home strongly when I went to the UK on a scholarship for a second MA. I was constantly in trouble with my bank for not moving money from the fixed to the spending account. So while I had the money, I had no idea how to use it.

Fast forward many years. As a young family trying to keep it all together with limited incomes and plenty of responsibilities, savings were difficult and but for the pressure of funding the wonderful middle Indian friend the Public Provident Fund (PPF), we would have been without savings.

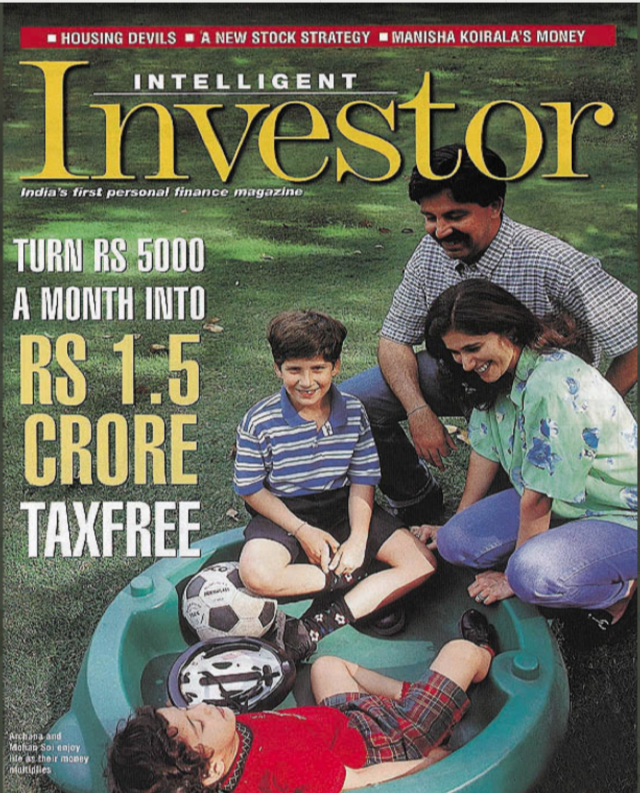

My real introduction to money happened when I joined what would be India’s first personal finance magazine, then called Intelligent Investor (now called Outlook Money). Sitting in the basement of AB10 Safdarjung Enclave, New Delhi, I had access to two wonderful things: the Internet and Excel. The year is 1997 and having an internet connection on your own computer at work is a luxury. This new tool opened the world of personal finance to me. The genre was unknown in India where business magazines were all about getting CEOs to put their knuckles on their chins to pose for cover stories. Personal finance put us, as individuals, on center stage as the heroes. As the protagonists. The world flipped over and I began to see it from the point of view of the average middle-class Indian and her money. When I used the insight of compounding and applied it to the PPF, compounding Rs 5,000 a month over 30 years, the results caused the top Outlook magazine bosses to fall off their chairs! At the then 12% return, the final sum was over Rs 1 crore. A huge big deal in 1997.

While I quickly became the person who knew a lot about personal finance, I soon realised that I actually knew very little. I remember, very long ago, when I was asked once what NAV stood for and I opened and shut my mouth. This triggered a whole new journey of learning, passing exams and getting equipped to actually be qualified to write on personal finance. I wanted to be 10 questions deep at least in the subject I was writing about. I voluntarily took the responsibility of being a fiduciary for my readers and viewers.

Then began a journey of decoding, explaining, informing, warning and advising people on money through various media – newspapers, magazines, TV shows and live events. The more I engaged with money, the more it spoke to me, the deeper I got into the space.

But as I got to know more. I got to understand the financial sector, regulations and how important it was to hardcode consumer protection into the regulatory rules of the game. And then began a long journey of trying to get the rules of the game changed for all of us. I worked with the government, worked pro bono on regulatory and government committees to put consumer protection and financial literacy on the map for decades.

There have been some wins and many losses in getting the market to move from a buyer-beware to a seller-beware place. And that battle continues till date.

While I keep pushing for a fairer marketplace at the policy level, I love to keep meeting real people to spread financial education deep and wide. I love to hear stories of real people living their lives and trying to make it all work.

Every time I hear from you and you tell me that you took a good financial decision or escaped some financial trap because of my books, workshop, video or writing, I feel as if I have won!

When you have a good money outcome. I win.